Yesterday's Fed meeting didn't just hold rates—it basically told every pool service business that cheap money isn't coming back anytime soon. The Federal Reserve kept rates at 3.50–3.75% and stripped out any language hinting at cuts, which means expensive borrowing costs through at least 2027.

For pool service owners heading into peak season, this creates a genuinely rough spot: truck loans, equipment financing, and working capital lines all stay expensive while chemical costs keep climbing and customers push back harder on any price increase you try to make stick.

I pulled data from 47 pool service companies we work with across Florida, Arizona, and Texas. The ones that held their margins through the 2022–2023 rate spike all did three things differently than the ones that struggled. They adjusted pricing methodically instead of reactively, changed how they managed inventory float, and restructured their staffing model before wage pressure forced their hand.

Why June's Fed stance hits pool services harder than other trades

Pool service businesses face a squeeze that most other service trades don't. Unlike HVAC or plumbing where emergency calls create real pricing power, pool maintenance is mostly recurring revenue at fixed monthly rates. You can't suddenly charge double because borrowing got more expensive.

The math gets ugly fast. A typical 15-truck operation in Phoenix carries around $280,000 in vehicle debt, another $45,000 in equipment financing, and needs $60,000–$80,000 in working capital during peak season. When rates jumped from 3% to 7%, that same debt load costs close to $1,900 more per month. Add chemical inflation running 8–12% annually and you're looking at roughly $2,400 in additional monthly costs that simply didn't exist three years ago.

What makes it worse is pool service has one of the longest cash conversion cycles in residential services. You buy chemicals today, apply them over the next 30 days, bill at month end, then wait another 15–30 days to collect. That 45–60 day float kills cash flow when rates are high.

The companies that adapted didn't just raise prices. They changed their operational model to actually work in a high-rate environment.

Pricing adjustments that actually stick with customers

Most pool service owners handle rate increases wrong. They wait until costs force their hand, then send a generic email about "rising costs" and hope customers don't cancel. That approach typically drives 12–15% churn based on cancellation data from companies that have tried it.

Eliminate missed appointments and dispatch delays.

Splshly ensures every pool service is scheduled, tracked, and completed efficiently.

- Unified scheduling dashboard

- Automated customer reminders

- Technician route optimization

No credit card required

There's a better sequence—three moves, done in order.

First, segment your customer base by margin contribution, not revenue. Pull your actual service time per pool, chemical usage, and drive distance. You'll find roughly 30% of your accounts are already unprofitable when you factor in real costs. These need immediate repricing or termination.

One company in Scottsdale found 89 of their 310 accounts were losing money—mostly large properties with heavy bather loads requiring double chemical doses but paying standard residential rates. They repriced these accounts 40% higher, lost 31 customers, and improved monthly profit by $3,200.

Second, implement variable pricing based on measurable factors. Instead of blanket increases, tie prices to specific cost drivers:

-

Distance from your service hub (fuel surcharge)

-

Pool size and type (chemical usage)

-

Equipment age (maintenance complexity)

-

Property access difficulty (time cost)

This lets you explain exactly why certain accounts cost more. Customers accept logic better than vague justifications.

Third, build a two-tier rate structure: locked rates for annual prepayment versus floating monthly rates. Offer customers who prepay annually a 5% discount and rate protection. It improves your cash position while giving price-sensitive customers an option besides canceling.

Inventory financing without killing cash flow

Traditional pool service inventory management was built around cheap capital—buy in bulk for discounts, stock heavy for peak season, carry 60–90 days of supplies. That model breaks when your business line of credit hits 9% APR.

The better approach is just-in-time practices adapted for seasonal patterns. Start with chemical purchasing. Instead of truckload quantities of tabs and shock, negotiate weekly delivery contracts with suppliers. Yes, you'll pay 8–10% more per unit, but you'll free up $20,000–$30,000 in working capital.

One Tampa operation restructured their entire chemical buying process around cash velocity. They moved from monthly bulk orders averaging $18,000 to weekly orders around $4,500. Per-unit cost went up by about $1,400 monthly, but they eliminated $14,000 in average carrying costs at 8.5% APR—net margin actually improved by roughly $200 while cash flow got dramatically better.

For equipment parts, a tiered stocking approach works well:

-

A-items (pumps, filters, common repairs)

Stock 14 days

-

B-items (automation, heaters)

Stock 7 days

-

C-items (specialized parts)

Next-day supplier agreements

This reduces parts inventory investment by roughly 40% without hurting service levels. The key is negotiating guaranteed next-day delivery agreements for C-items, even if it costs a small premium.

Track inventory turns. In a high-rate environment, every dollar tied up in inventory costs you 8–9% annually. Most pool services turn inventory 6–8 times per year. Push for 12+ turns on chemicals and 10+ on common parts.

Negotiate guaranteed next-day delivery agreements for C-items even if it costs a small premium; it preserves cash without disrupting service.

In a high-rate environment, every dollar tied up in inventory costs you 8–9% annually. Most pool services turn inventory 6–8 times per year. Push for 12+ turns on chemicals and 10+ on common parts.

Staffing model changes for sustained wage pressure

The CNBC analysis of the Fed's statement notes that wage growth remains "uncomfortably high" at 4.2% annually. For pool services competing against Amazon warehouses and construction sites for workers, the pressure is often worse—6–8% wage inflation annually isn't unusual.

The old model of hiring experienced techs at market rate doesn't pencil out anymore. A certified pool operator in Phoenix commands $28–32 per hour. Five years ago, that same role paid $19–22. You can't absorb a 45% labor cost increase through price increases alone.

The companies that figured this out restructured around apprenticeship and technology leverage. Instead of hiring five experienced techs at $30/hour, hire three experienced techs at $32/hour and four apprentices at $18/hour. Pair each apprentice with a senior tech for the first 90 days, then move them onto simple maintenance routes.

The economics work because pool maintenance follows the 80/20 rule—roughly 80% of visits only require basic chemical testing and adjustment that apprentices can handle after proper training. Reserve experienced techs for equipment repairs, new customer onboarding, and problem pools.

Apprenticeship alone isn't enough, though. You need operational software that lowers the skill floor for basic tasks. When techs can follow step-by-step diagnostic workflows on a tablet, scan chemical readings directly into the system, and pull up equipment-specific guides on the spot, you can run leaner on experienced staff. A 200-pool route that traditionally needed four experienced techs can operate with two seniors and three apprentices when properly supported by AI-powered operational software. That's around $64,000 in annual labor savings, even accounting for slightly slower service times.

Operational moves most owners miss

Beyond pricing, inventory, and staffing, a few quieter operational changes move the needle in a high-rate environment.

Rethink your service area geography. Every mile driven costs more when fuel stays elevated and vehicle financing runs 7–8%. Plot customer density by ZIP code and calculate revenue per square mile. You'll likely find 20–30% of your territory generates negative margin once you account for drive time and fuel.

A Tucson operation analyzed their 14-ZIP coverage area and found three ZIPs with fewer than eight customers each, requiring 45+ minutes of daily windshield time. They gave those customers a choice: accept a $40 monthly surcharge or transfer to a competitor. They lost 19 accounts but cut $1,100 in monthly vehicle costs.

Equipment replacement math changes too. High interest rates shift the rent-versus-buy calculation. An $8,000 variable-speed pump installation might make more sense as a $180 monthly rental agreement when your cost of capital exceeds 8%.

A simple decision matrix helps here:

| Expected Equipment Life | Decision |

|---|---|

| Under 3 years | Always rent |

| 3–5 years | Rent if customer credit is questionable |

| Over 5 years | Finance only for reliable, long-term customers |

This reduces working capital requirements while pushing credit risk to equipment suppliers who have better collection infrastructure than most pool service operators.

Also look at service frequency. Most pool services default to weekly service year-round, but plenty of pools can hold quality with bi-weekly service during winter months, especially with chemical automation. Offering seasonal frequency adjustments can cut route costs 20–25% during slow months without losing the customer relationship.

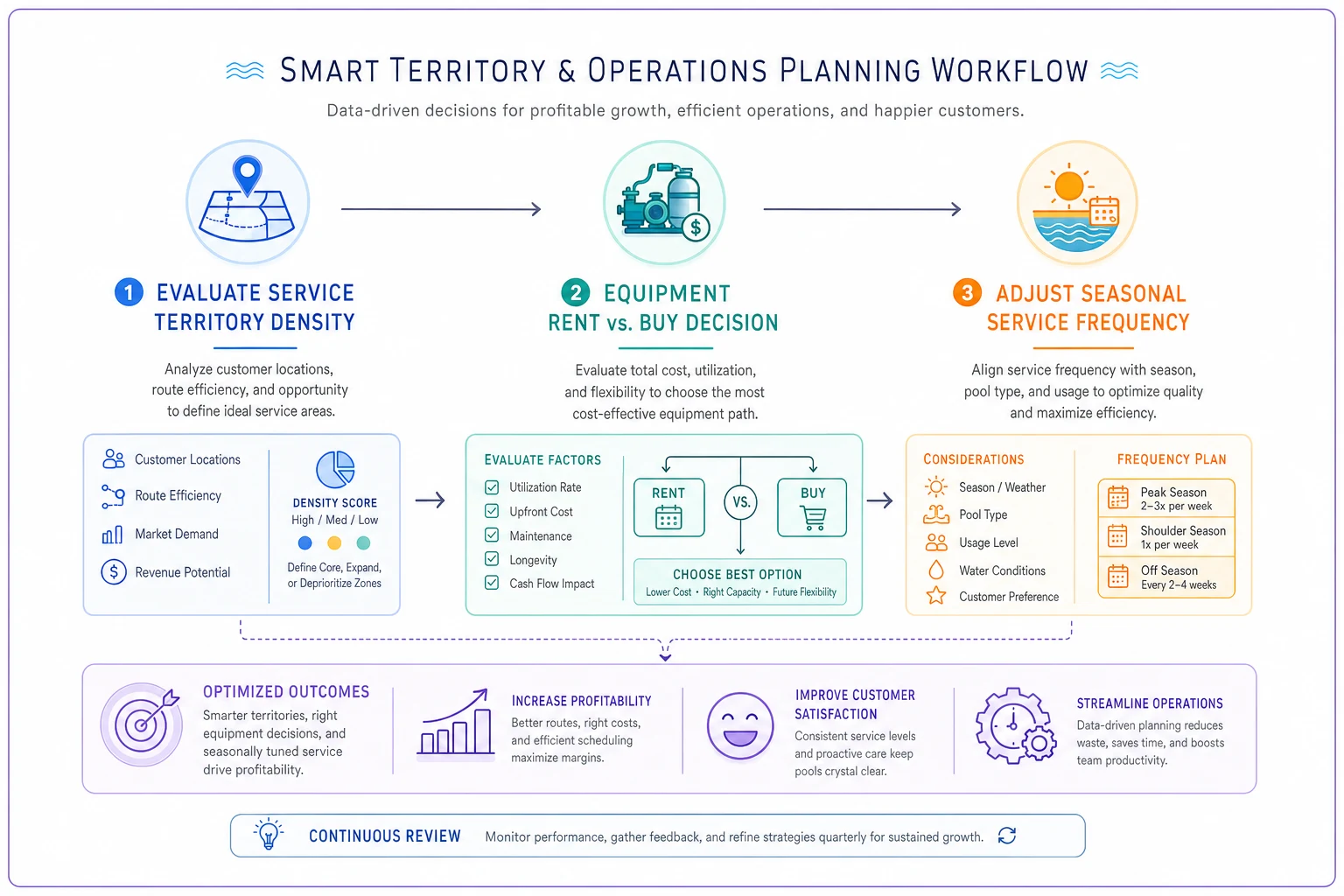

Here's a quick visual of the decision workflow for territory, equipment, and frequency choices.

Use this workflow to prioritize changes that cut capital intensity without disrupting core service delivery.

Cash preservation tactics for the long haul

The Fed's "higher for longer" posture means cash management starts to feel like survival management. Every excess dollar of cash costs you the spread between your savings rate (roughly 4%) and your line of credit rate (8–9%). Running too lean creates real operational risk though.

Bucket 1: Operating cash (1.5 months of expenses) Keep this in your business checking for daily operations. Any excess sweeps to Bucket 2 nightly.

Bucket 2: Reserve cash (1 month of expenses) Park this in a money market account earning 4–5%. Buffers seasonal swings and unexpected repairs.

Bucket 3: Growth cash (varies) Only build this after Buckets 1 and 2 are full. Use for equipment upgrades, route acquisitions, or paying down high-interest debt early.

Most owners keep too much sitting in Bucket 1, earning nothing, while carrying credit card balances at 18% APR. That spread costs 14% annually on every excess dollar—it adds up faster than most people realize.

Renegotiate payment terms with every vendor. Push for 45–60 day terms on supplies and equipment. Even if you pay a 2% premium for extended terms, you come out ahead when your cost of capital exceeds 8%. It's essentially free financing from vendors who have better credit access than most small operators.

Accelerate collections through payment automation. Manual billing and check collection typically produces 38–45 day receivables. Automated card processing drops that to 1–3 days. The 3% processing fee is worth it at current rates. A typical $80,000 monthly billing operation frees up around $26,000 in working capital by moving to automated payments.

Technology investment that pays back in this rate cycle

High interest rates actually make certain technology investments more attractive, not less. When labor costs 6–8% more annually and working capital costs 8–9%, any system that cuts headcount or speeds up cash flow pays for itself quickly.

The highest ROI typically comes from AI-powered operational platforms that handle scheduling, routing, inventory tracking, and customer communication. These usually run $200–$400 per month for a smaller operation but eliminate 10–15 hours of administrative work weekly.

More importantly, they reduce the skill level needed for basic operations. When your system automatically calculates chemical doses based on test results, generates optimized routes, and tracks inventory levels in real time, you can run with fewer experienced staff. The labor arbitrage alone—replacing a $25/hour office manager with a $16/hour coordinator supported by the right software—saves around $1,500 monthly.

Choose platforms built specifically for pool service, not generic field service tools. Pool service has unique requirements around chemical tracking, water testing documentation, and seasonal scheduling that general platforms handle poorly. The extra cost for a specialized platform pays back through fewer errors and faster onboarding.

That said, avoid over-automating. Some owners buy every possible software tool and create complexity that needs more management, not less. Focus on three core areas: scheduling and routing, chemical and inventory management, and customer billing and communication. Everything else is optional.

Margin protection checklist for the next 18 months

Based on the Fed's signaling and current conditions, assume rates stay elevated through at least mid-2027. Here's a prioritized action list:

Immediate (next 30 days):

-

Analyze customer profitability and identify losing accounts

-

Renegotiate vendor payment terms for 45+ days

-

Move monthly chemical orders to weekly delivery

-

Calculate true cost per service visit including windshield time

Short-term (next quarter):

-

Implement tiered pricing based on service complexity

-

Reduce parts inventory by 30–40% through supplier agreements

-

Convert 50%+ of customers to automated payment processing

-

Eliminate or surcharge unprofitable service territories

Medium-term (next 6 months):

-

Restructure staffing toward the apprenticeship model

-

Deploy operational software for routing and inventory

-

Offer prepaid annual contracts with rate protection

-

Establish equipment rental programs for major repairs

Long-term (12–18 months):

-

Build cash reserves to 2.5 months of expenses

-

Develop winter service options to smooth revenue

-

Consider acquiring struggling competitors at discounted valuations

-

Prepare for potential consolidation in your market

The pool service companies that come out ahead during this stretch of expensive money won't be the ones that raise prices and hope for the best. They'll be the ones that actually restructure for capital efficiency.

What this means for your business model

The Fed's June stance is essentially announcing that the cheap money era is over for the foreseeable future. For pool service businesses built on assumptions of 3–4% interest rates and stable labor costs, that means rethinking a lot—pricing strategy, operational structure, staffing ratios, inventory habits.

The successful adaptation isn't about dramatic changes. It's about dozens of smaller adjustments that compound into sustainable profitability. Every operational decision now has to factor in the cost of capital. Every staffing choice needs to account for persistent wage inflation. Every customer relationship needs to generate real margin, not just revenue.

The companies that navigate rate cycles like this tend to share a few common traits: they make decisions based on actual data, they prioritize cash flow over growth, and they invest in systems that reduce dependence on expensive skilled labor.

Your ability to manage seasonal capacity and cash flow becomes even more critical when capital is expensive. The margin for error shrinks, but the opportunity for well-run operations to take market share from struggling competitors is real.

The next 18 months will likely see meaningful consolidation in the pool service industry. Companies that restructure now will be buying out the ones that didn't—often at attractive prices. The Fed just told us rates aren't dropping soon. The only real question is whether you adjust fast enough to be on the right side of that consolidation.

Ready to elevate your pool service business?

Join hundreds of pool service professionals using Splshly to save time, optimize routes, and enhance customer satisfaction.